Ch.3 Reconstitution of a Partnership – Admission of a Partner

- . Reconstitution of a partnership happens at the time of ______.

(a) Admission of a partner (b) Retirement of a partner (c) Death of a partner (d) All of these

Ans : (d) All of these - X and Y are partners sharing profits in the ratio 3 : 2. They admit Z into partnership with 1/5 share in future profits. What will be the sacrificing ratio ?

(a) 3 : 2 (b) 2 : 1 (c) 1 : 1 (D) 3:1

Ans : (a) 3 : 2 - What do you mean by goodwill ? List out any 2 factors affecting goodwill. (3Marks)

Ans : Goodwill

Goodwill the value of reputation of a firm in respect of the profits expected in future over and above the normal profits earned by other similar firms belonging to the same industry.( One score for meaning)

Factors affecting the value of goodwill (Any Two points – One score each. Max. 3 scores)

1) Favorable Location

2) Nature of business

3) Efficiency of management

4) Market situation

5) Special advantages

6) Time Factor

- Amala and Nandana are partners in a firm sharing profits and losses in the ratio of 3 : 2. They decided to admit Hajara as a new partner for 1/5th share in profits,which she acquired equally from Amala and Nandana.Calculate the new ratio after admission. (3 Marks)

Ans :

Old Ratio of Amala and Nandana= 3:2

Hajira’s share = 1/5 (acquired equally(1/10 each) from old partners

So, Amala’s New share = 3/5 – 1/10 = (6/10-1/10) = 5/10 ( 1 score)

Nandana’s new share = 2/5 – 1/10 = (4/10- 1/10) = 3/10 ( 1 score)

Hajira’s share = 1/10+1/10 = 1/5 or 2/10 ( 1⁄2 score)

New ratio of Amala, Nandana and Hajira = 5:3:2 ( 1 1⁄2 scores) - Kareem and Raheem are partners in a firm sharing profits in the ratio 2 : 1. They admit Jacob into partnership. Kareem surrenders 1/4 of his share and Raheem 1/2 of his share in favour of Jacob. Calculate the new profit sharing ratio. (2 Score)

Ans : 3:1:2 - Neena and Meera are partners in a business. Their total capital of the firm is ` 1,20,000.The normal rate of return on similar type of business is 10%. The actual profits for the three years were ` 34,000, ` 40,000 and ` 46,000. Calculate the value of goodwill if goodwill is valued at 2 years purchase of the last 3 years average super profit. (3 Score)

Ans: Normal Profit : 12,000.Average Profit – 40,000

Super profit – 28,000

GW -28000*2 = 56000 - Goodwill brought in by the incoming partner in cash is credited to _______.

(a) Old Partners Capital Account in Sacrificing ratio

(b) Old Partners Capital Account in new ratio

(c) New Partners Capital Account in Gaining ratio

(d) New Partners Capital Account in new ratio

Ans : (a) Old Partners Capital Account in Sacrificing ratio

- At the time of reconstitution of a firm the value of Building is found appreciated by 20%. What journal entry will be passed for above adjustment with regard to revaluation ?

Ans : Building A/c Dr

To Revaluation A/c - Briefly explain any two circumstances which need for valuation of goodwill in a Partnership firm. (2 score)

Ans :

1 – Change in the profit sharing ratio of partners

2 – Admission of a Partner

3 – Retirement of a Partner

4 – Death of a Partner

5 – Dissolution of Partnership firm

6 – Amalgamation of firms - Enumerate any two rights acquired by a newly admitted partner of a firm. (2 score)

Ans :

1 – Right to share the Assets of the firm

2 – Right to share the Profits of the firm - Abhinav and Adarsh are partners in a firm sharing profits and losses in the ratio of 5 : 3. Ananya is admitted in the firm for 1/5th share of profits. She has to bring in 20,000 as capital and 4,000 as her share of goodwill. Give the necessary journal entries if the amount of goodwill is retained in the business.

Ans : Journal Entries – Treatment of Goodwill:

(i) Cash A/c Dr. 20,000

To Ananya’s Capital A/c 20,000

(ii)Cash A/c Dr. 4000

To Goodwill A/c 4,000

(Capital and Goodwill brought in by Ananya)

(ii) Goodwill A/c Dr. 4,000

To Abhinav’s Capital A/c 2,500

To Adarsh’s Capital A/c 1,500

(Goodwill transferred to old partners in the ratio of 5:3)

( 2 scores for entry – 2 scores may be awarded for the calculation of sacrificing ratio, Max.4 scores)

- The profits for 5 years of a firm are as follows :

2013 – ` 12,000

2014 – ` 18,000

2015 – ` 17,000

2016 – ` 14,000

2017 – ` 24,000

Calculate goodwill of the firm on the basis of 3 years purchase of 5 years average profits.

Ans : . Total Profit = 12000+18000+17000+14000+24000 = 85,000

Average Profit 85000/5 = 17,000

Goodwill = 3 years purchase of the average profit ie. 17000 x 3 = 51000

( One score for Total profit, Two scores for Average Profit, Two scores for Goodwill- Max. 5 scores)

- What are the different modes of reconstitution of a partnership firm ? Briefly explain.

Ans:

Modes of Reconstitution of a Partnership Firm: 5

1. Change in the profit sharing ratio among the existing partners

Sometimes partners of an existing firm may decide to change their existing profit sharing ratio.The change in profit sharing ratio may lead to increase or decrease partner’s share in the firm. In other words, certain partner may gain others will lose.

2. Admission of a new partner

Inclusion of a person as a partner to an existing partnership firm is called admission of a partner. When a firm requires additional capital or managerial help or both for the expansion of its business, a firm can admit a person as a partner to an existing firm.

3. Retirement of a partner

Retirement means withdrawal of a partner from an existing business. Retirement may be due to his bad health, old age or change in business interests.

4. Death of a partner

Death of a partner will also result in the change of relationship between surviving partners. Their profit sharing ratio will change and it leads to reconstitution.

5. Amalgamation of two firms

Sometimes two firms amalgamate in order to avoid competition and reduce administrative cost.This arrangement brings new relationships among partners of two firms. A new agreement is signed. New profit sharing arrangements takes place. Here also reconstitution occurred.

( One score each for brief explanation of points – 1⁄2 scores each for points only- Max. 5 scores)

- Abhirami and Dayana are partners in a firm sharing profits and losses equally. Their balance sheet as on 31st Dec. 2018 were as follows :

They decided to admit Manju as a partner on that date for a 1/4 share in profit and

the following were agreed upon :

(i) Manju contributed ` 20,000 as capital and ` 10,000 as her share of goodwill.

(ii) Furniture is valued at ` 28,000.

(iii) Land and buildings found appreciated by 10%.

(iv) A provision of 5% on debtors were created for bad debts.

Prepare the Revaluation account and Capital account of the firm after admission.

Ans : Revaluation loss 2400 ( 1200+1200)

Capital Ac Balance Abhirami – 40800, Dhanya – 42800, Manju – 20000

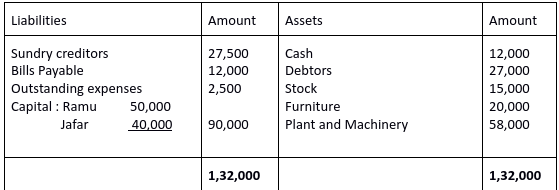

- Given below is the Balance Sheet of Ramu and Jafar who were sharing Profits and Losses in the ratio of 3 : 2 as on 31st December, 2015. (2020 SAY)

Shoby is admitted as a partner on the date of Balance Sheet on the following terms :

(a) Shoby will bring ` 30,000 as capital and ` 12,000 for his share of goodwill for ¼ share in profits.

(b) Plant and Machinery is depreciated by ` 8,000.

(c) Stock is found overvalued by ` 3,000.

(d) A provision for doubtful debts is to be created at 10% on debtors.

(e) Creditors were unrecorded to the extent of ` 1,000.

Prepare Revaluation Account, Partners Capital Account and the new Balance Sheet after the admission of Shoby.

Ans : Revaluation Loss : 14700 ( Ramu – 8820,Jafer-5880)

Capital A/c Balance Ramu – 48380, Jafer – 38920, Shoby – 30,000)

- The profit for the last five years of a firm were as follows :

Year Profit

2014 62,000

2015 58,000

2016 84,000

2017 78,000

2018 80,000

Capital employed in the firm is ` 5,00,000. Calculate the value of goodwill on the basis of 3 years purchase of Super Profit, assuming that the normal rate of return on capital employed is 12%.

Ans : 1 – Average profit = 362000/5=72400

2 – Normal profit = 500000*12/100=60000

3 – Super profit – 72400-60000=12400

4 – Goodwill = 12400*3 =37200

- Sathy and Varsha are partners in a firm sharing profit and losses in the ratio of 3 : 1. Their Balance Sheet as on 1st January 2019 was as follows :

Suma is admitted into the firm with 1⁄4 share in profits on the following terms :

(1) Market value of Investment are to be taken at ` 70,000.

(2) Buildings were found undervalued by ` 4,000.

(3) Stock is revalued at ` 26,000.

(4) It was found that creditors included a sum of ` 3,000 which was not to be paid.

(5) Machinery is to be depreciated by 10%.

Prepare Revaluation Account. (5 Marks)

Ans : Revaluation profit – 16000 (Sathy – 16000, Varsha – 4000)

- Complete the following Journal Entry :

_________________________ A/c. Dr.

To Cash A/c.

(The amount of goodwill brought in by the new partner withdrawn by the existing partners.)

Ans: Old partners capital A/c Dr

- The profits earned by a business firm during the last 4 years were ` 90,000,80,000, ` 1,20,000 and ` 1,10,000 respectively. Normal rate of return in similar business is 8%. Calculate the value of goodwill by capitalization of average profit. Assume that the value of net assets is ` 9,00,000.

Ans : Average profit – 100,000

Capitalisation of Average profit = 100000*100/8 =12,50,000

Goodwill = 12,50,000 – 900000= 3,50,000

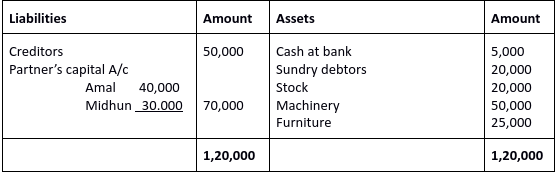

- Given below is the Balance Sheet of Amal and Midhun who share profits and losses in the ratio of 3 : 2.

Mr. Faisal is admitted into the partnership on the following terms :

(i) New partner has to bring in ` 25,000 as capital and ` 10,000 as goodwill for 1/6th share.

(ii) A creditor of ` 1,000 will not claim his amount.

(iii) Furniture is revalued at ` 20,000.

(iv) Stock reduced by ` 2,000.

(v) Depreciation on machinery @ 10% p.a.

Prepare the Revaluation A/c., Partners’ Capital A/c. and the Balance Sheet after admission.

Ans : Revaluation loss – 11000 ( Amal – 6600,Midhun – 4400)

Partner’s capital A/c

Amal kc -39400

Midhun -29600

Faisal – 25000

Balance sheet total :143000

- on admission of a partner, the Debit Balance of Profit and loss account shown in the Balance Sheet of the firm, denotes :

(a) Accumulated Profit

(b) Accumulated Loss

(c) Revaluation Loss

(d) General Resele

- The proportion in which existing partner surrender their share of profit in favor of newly admitted partner is called :

(a) Sacrificing ratio (b) Gaining ratio (c) Old ratio (d) New ratio

- Arun and Babu are partners in a frim sharing profit and losses in the ratio of 3 : 2. They admitted Chandu as a partner for 1/6 share with a guaranteed minimum profit of Rs.15,000 The Net profit of the firm for the year ending 31st March, 2021 was ` 60,000. Chandu’s share of profit will be :

(a) ` 10,000 (b) ` 15,000

(c) ` 20,000 (d) ` 30,000

- The capitalized value of average profit of a business is ` 5,00,000 and value of net assets of the business is ` 4,20,000. The Goodwill of the business under capitalization method will be

(a) Rs. 5,00,000 (b) Rs.4,20,000

(c) Rs. 80,000 (d) Rs.9,20,000

- State any two circumstances under which goodwill of a partnership firm is valued. Smitha and Varghese are partners sharing profits in the ratio of 2 : 1. They admitted Soorya as a new partner for 1/4share in the future profits of the firm. Calculate new profit sharing ratio of Smitha, Varghese and Soorya.

- The share of goodwill brought in by the new partner is shared by the old partners in their _______.

(a) Old ratio (b) Sacrificing ratio (c) New ratio (d) Ratio of their capitals

- Goodwill existing in the books at the time of admission of a partner is transferred to the capital accounts of _____.

(a) old partners in sacrificing ratio (b) all partners in new ratio (c) old partners in old ratio (d) all partners in capital ratio

- State any four circumstances which require the valuation of goodwill.

Ans : Change in profit sharing ratio

Admission of a partner

Retirement and death of a partner

Dissolution of partners ship

Amalgamation of partnership

- Balu and Binu are partners in a firm sharing profits in 5:3 ratio. They admit Babu as a new partner and the new profit sharing ratio was agreed at 4:2:1. Calculate the sacrificing ratio.

Ans : SR 3:54 - Lalu and Balu were partners in a firm sharing profits and losses in the ratio of 3:1. They admitted Jisha as a new partner for 1/5 share. Jisha brings ` 1,00,000 as capital and ` 20,000 as her share of goodwill. On the date of Jisha’s admission the balance sheet of the firm showed a balance of ` 10,000 in Reserve Fund. Record necessary journal entries for the treatment of these items on Jisha’s admission.

- The profit of a firm for the last four years are as follows :

Year Profit

2018 – 10,000

2019 – 15,000

2020 – 20,000

2021 – 30,000

Calculate the value of goodwill on the basis of 2 years purchase of weighted average profits based on weights 1, 2, 3 and 4.

Ans: GW – 44000

- Following is the Balance Sheet of Leena and Jyothi who share profits in the ratio of 3:1 as on 31 March, 2021.

Rajesh is admitted as a partner on the date of the balance sheet as per the following terms :

1. Rajesh will bring in ` 1,00,000 as his capital for 1/5 share in profits.

2. Plant & Machinery is to be appreciated to ` 60,000 and the value of buildings is to be reduced by 10%.

3. Stock is revalued at ` 20,000.

4. Investment worth ` 2,500 is to be taken into account.

Prepare Revaluation Account.

Ans: Revaluation Profit – Leena – 7875, Jyothi – 2625

- If an incoming partner brings the premium of goodwill in cash, it will be shared by the old partners in :

(a) new profit sharing ratio (b) old profit sharing ratio (c) capital ratio (d) sacrificing ratio

Ans :sacrificing ratio

- Calculate the value of goodwill under capitalization method.

Average profit of the last 5 years: Rs.40,000

Normal rate of return in similar business : 10%

Total assets: Rs.5,00,000

Outside liabilities: Rs. 1,80,000

Ans:80000

- Hartha and Samitha are partners in a firm sharing profits and losses in the ratio of 5:3. The following is their balance sheet as on 31 st march 2018.

Balance sheet as on 31 St march 2018

| Liabilities | Amount | Assets | Amount |

| CreditorsGeneral reservedCapital : Harithasamitha | 32,0008,000 40,00030,000 | Bank AccountsBills receivablesDebtors 18,000 Less Provision 1500StockFurnitureLand & Building | 12,0002,500 16,50017,00022,00040,000 |

| 1,10,000 | 1,10,000 |

They decided to admit Sameera into partnership on 1st April 2018 on the following terms.

- That sameera has to bring Rs.25,000 as capital for ¼ share in future profits.

- That sameera will bring her share of Goodwill Rs.9000

- The value of land and Building be appreciated and brought upto Rs.45,000

- Furniture to be reduced by 10%

- Stock revalued by 10%

- Creditors of Rs.2000 are not likely to be claimed.

Prepare Revaluation Account, the capital Accounts of Partners and Balance sheet of the new firm.

Ans : Rev. Profit – 3800, Capital – 53000,37800,25000 B/s – 145800

- A and B are partners in a firm sharing profits in the ratio 3 : 2. They decided to admit C into partnership for 1/4 share in profits. C will bring in ` 30,000 for capital and required amount for goodwill premium in cash. The goodwill of the firm is valued at ` 20,000. The new profit sharing ratio is 2 : 1 : 1. Give journal entries.(june 2023)

Ans : 5000, SR 2:3, 200,3000

- Ajay and Vijay were partners in a firm sharing profits in the ratio 3 : 2. On 1-1-2022 they admitted Sujay into partnership for 1/5 share of profits. The balance sheet on 31-12-2021 was as follows :

Balance Sheet as on 31-12-2021

| Liabilities | Amount | Assets | Amount |

| Bank OverdraftCreditorsReserveCapitalAjayVijay | 10,00015,00010,000 80,000030,0000 | CashDebtors – 22000Less : Provision 20000StockPlantLand and Building | 5,000 20,00030,00035,00055,000 |

| 1,45,000 | 1,45,000 |

It was agreed that

(a) The value of Land and Building is increased by ` 15,000.

(b) The value of Plant is reduced by ` 10,000.

(c) The provision for doubtful debt is to be increased by ` 1,000.

(d) Sujay has to bring in ` 50,000 as capital and ` 4,000 as premium for goodwill.

Prepare Revaluation Account, Partners Capital Account and Balance Sheet after the admission of Sujay. (Say 2023 )

Ans : Revaluation Profit : 6000 , (2400,1600) Capital Acs ,Ajay-90800,Vijay – 37200,Sujay -50000, B/s – 2,03,000)