DISSOLUTION OF PARTNERSHIP FIRM

Dissolution means breaking up or undoing.There are two types of Dissolution:-

1-Dissolution of Partnership

Dissolution of partnership changes the existing relationship between partners but the firm may continue its business as before.It takes place in the following circumstances.Here business is not closed.

- Changes in PSR among partners

- Admission of a new Partner

- Retirement/Death of a partner

- A partner becomes insolvent etc

- Completion the venture

- Expiry of the period of partnership

2-Dissolution of a Firm

When the partnership between all the partners of a firm comes to an end ,it is called dissolution of a firm.When the firm is dissolved , it leads to the closure of the business.

Modes of the dissolution of a firm

- Dissolution by agreement

A firm is dissolved

a) With the consent of all the partners

b) As per the terms of the partnership agreement

- Compulsory dissolution

A firm is dissolved compulsorily in the following cases:

a) When the business of the firm becomes illegal

b) When all the partners or all except one become insolvent

c) When all the partners or all except one decides to retire from the firm

d) When all the partners or all except one die

- On the happening of certain contingencies

In the absence of an agreement to the contrary, a firm will be dissolved in the following cases:

a) If constituted for a fixed period, by the expiry of that term

b) If constituted to carry out one or more ventures, by the completion thereof;

c) By the death of a partner

d) By the declaration of a partner as an insolvent

- Dissolution by notice

If any one of the partners gives a notice in writing to other partners, signifying his intention to dissolve the firm.

- Dissolution by court

a) When a partner becomes of unsound mind

b) When a partner becomes permanently incapable of performing his duties as a partner

c) When the partner transfers all of his interest in the firm to a third party

d) When the business of the firm is can’t be carried on at a loss.

e) When the partner commits breach of agreement relating to the management of the firm

f) When, on any ground, the court regards dissolution to be just and equitable

Distinction between Dissolution of Partnership and Dissolution of Firm

| Basis | Dissolution of partnership | Dissolution of Firm |

| 1-Termination of business | Business is not terminated | The business is terminated |

| 2-settlement of Assets and liabilities | Assets and liabilities re valued and new B/S prepared | Assets are sold,liabilities are paid off and balance utilised towards settlement of partners |

| 3-Court intervention | Court does not intervene.Dissolution of partnership by mutual agreement | A firm can be dissolved by the court order |

| 4-Economic relationship | Economic relationship still continues,but with some changes | Economic relationship among the partners comes to an end |

| 5-Closure of books | Books of accounts are not closed as the business is not terminated | All books of accounts are closed as business is terminated |

Settlement of Accounts

In case of dissolution of a firm, the business is discontinued and the firm has to settle its accounts.For this purpose , all the assets of the firm are sold and liabilities are paid off and the balance available is distributed amongst the partners.

a) Losses shall be paid first out of profits ,next out of capital, and lastly ,if necessary ,by the partners individually in the proportion of their profits sharing ratio.

b) The assets of the firm shall be settled in the following manner and order

Order of settlement of Accounts

- In paying the realisation expenses

- In paying the debt of the firm to third parties

- In paying repayment of loans from partners.

- In paying repayment of capital contributed by partners.

- The balance amount shall be divided among the partners in the Profit sharing ratio

Firm’s Debt and Private Debts

Firm’s debts are paid first out of the firm’s assets and if any balance can be used to meet Partner debts.

Partners Debts should be paid off first out of their private properties and if there is any balance it can be used to meet the firm’s debt.

The following accounts are prepared for the purpose of dissolution

2-Capital accounts of Partners:– Each partner’s capital account is credited with accumulated profit and realisation profit or debited with accumulated loss and realisation loss if any.The balance in the capital account represents the amount due to or due from each partner.It is closed by paying off or bringing in cash as the case may be.

3-Cash/ Bank Account:- After entering the cash realised and paying towards the liabilities and realisation expenses, the balance in this account equals the balance in the capital accounts of partners. When final account settlement is made cash account and partners capital account will automatically closed.

Loan from a partner

Loan from a partner is not transferred to realisation account.It is paid directly the loan accountitself.Loan from wife of a partner is treated as outside liability hence it is taken in to realisation account.

For payment of loans due to partners

Partners loan A/c Dr

To bank A/c

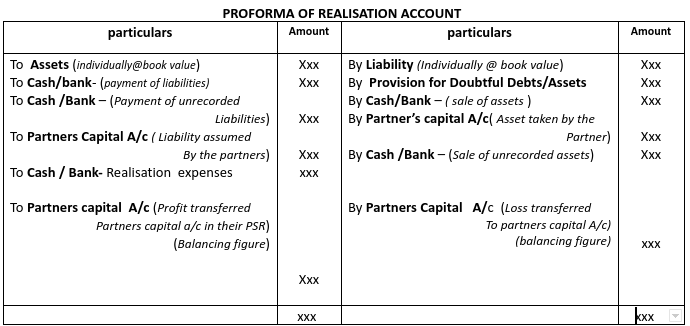

1-Realisation Account

It is a Nominal account prepared for the purpose of closing the accounts of assets and liabilities and finding out the profit or loss on realisation of assets and liabilities.

Journal Entries

1-For closing assets accounts- except cash, bank and fictitious assets

Realisation A/c Dr

To Assets A/c (Individually)

Note: Sundry debtors should be transferred at its full value without deducting the Provisions for doubtful debts.

2- provisions

Provision for Doubtful Debts A/c

“ Depreciation A/c

Joint life policy reserve A/c

Contingency Reserve A/c

Contingency Reserve A/c

Investment fluctuation fund A/c

To Realisation A/c

3-For closing liabilities account

All outsiders liabilities are closed by transfer to Realisation A/c

Sundry Creditors A/c

B/P A/c

B/P A/c

Bank O/D A/c

Outstanding exp: A/c

Partner’s wife’s loan A/c

Partner’s wife’s loan A/c

To Realisation A/c

4-For sale of Assets

Cash / Bank A/c Dr

To Realisation A/c

5-For assets taken over by a partner

Partners capital A/c Dr

To Realisation A/c

6-For payment of Liabilities

Realisation A/c Dr

To Cash / bank A/c

7- If a partner agree to discharge the liability

Realisation A/c Dr

To Partner’s capital A/c

8-For the amount realised from unrecorded asset or new asset including goodwill if any

Cash / Bank A/c Dr

To Realisation A/c

9-For payment of a Unrecorded or new liability

Realisation A/c Dr

To Cash/ Bank

10-For Transfer of profit or loss on realisation

In case of profit on realisation

Realisation A/c Dr

To Partner’s capital A/c (Individually@PSR)

In case of loss on realisation

Partners capital A/c (Individually)

To Realisation A/c

11-For transfer of accumulated profits in the form of Reserve fund or general reserve:

Reserve fund/General reserve A/c Dr

To Partner’s capital A/c(Individually)

12- For settlement of Partner’s accounts

The balance is paid to partners whose capital A/cs show a credit balance

Partners Capital A/cs Dr (Individually)

To Bank A/c

If the partner’s capital a/c shows a debit balance, he brings the necessary cash

Bank A/c Dr

To Partners Capital A/c

Goodwill on Dissolution of a Firm

1 – If it appears in the balance sheet ,it is transferred to the realisation account like any other assets.

2 – If it doesn’t appear in the balance sheet, it is not to be calculated.

Note:

- If nothing is mentioned regarding the realisation of an asset,it is assumed that the same asset is realised in full.

- If payment regarding any liability is not mentioned it is assumed that it is paid in full.

- If some specific funds like Investment fluctuation fund,workmen’s compensation funds ,joint life policy fund etc are given they should be credited to realisation account.This is because some losses or liabilities are attached to such funds.

- Provident fund is usually transferred to realisation A/c (Credit side).It is to be paid off (Debit side) through realisation A/c

General purpose funds such as General reserve, Reserve fund etc are directly credited to to capital accounts of the partners.

| Revaluation Account | Realisation Account |

| 1 – Prepared at the time of admission,retirement or death of a partner 2 – Prepared to show the assets and liabilities at their revised value and to know the profit /loss arising therefrom 3 – Only the changes (increase or decrease) in the value of assets and liabilities are recorded 4 – No expenses are shownFirm continue even after its preparation. | 1 – Prepared at the time of dissolution of a partnership firm 2 – Prepared to know the profit/loss on the sale of assets and payment of liabilities. 3 – Assets and liabilities are shown at the book value. 4 – Realisation expense are shown 5 – Firm is dissolved after its preparation. |