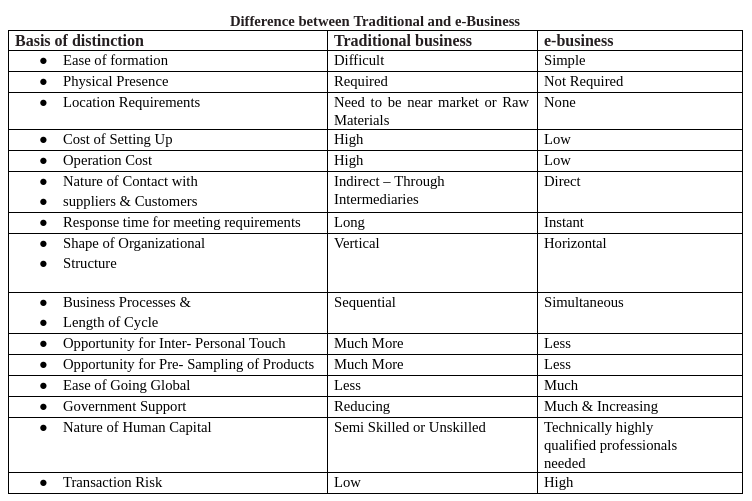

e-Business: e-Business may be defined as the conduct of industry, trade and commerce using the computer networks. Almost all types of business functions as well as managerial activities can be carried out over computer networks.

E-Commerce: It covers a firm’s interactions with its customers and suppliers over the internet. It is only a part of e-Business.

Scope of e-Business:

Firm’s e-business transactions can be seen in the following four ways:

1. B2B Commerce: In this commercial transactions take place between different business organizations. It include placing of purchase orders, invoices, quotations… Business to Business(B2B) form major share of total e-commerce volume.

2. B2C Commerce: It means Business to Customers transactions. It include selling of goods, call centers, ATM facility….

3. Intra-B Commerce: Here the transactions takes place with in the firm. It include use of computer networks in marketing, finance, production, purchase, human resource, Research and Development departments…. It also include interaction of business with its employees (B2E).

4. C2C Commerce: It means Customer to Customer. This type of commerce is best suited for dealing in goods for which there is no established market mechanism. The vast space of the internet ( eBay.com, olx.com, amazon.com, flipkart) allows persons to globally search for potential buyers.

Benefits of e-Business:

1. Easy of formation and lower investment requirements: It is relatively easy to start due to less legal procedure. Even if you do not have much of the investment, you can do the business through network.

2. Convenience: Internet offers the convenience of 24 hours business.

3. Speed: Internet allows faster services.

4. Global reach: It provides a boundary less market.

5. Movement towards a paperless society: Use of internet has considerably reduced dependence on paperwork.

6. Lower transaction cost

7. It provide quality services

8. It provides new/innovative business opportunities.

Limitations of e-Business:

1. Low personal touch

2. Physical delivery of the product takes time.

3. Need for technology capability and competence of parties to e-business. 4. Can be used by dishonest people for illegal activities.

5. Information exchanged through internet may be stolen or misused.

6. People resistance

7. Ethical fallouts

Online transactions:

Three stages involved in online transactions- pre purchase/sale stage, purchase/sale stage and delivery stage.

Procedure:

a. Registration: Before online shopping, one has to register with the online vendor by fulfilling-up a registration form.

b. Placing an order: You can pick and drop the items in the shopping cart. Shopping cart is an online record of what you have picked up while browsing the online store.

c. Payment mechanism: Payment for the purchases through online shopping may be done in a number of ways such as-Cash on Delivery(CoD), cheque, net banking, credit/debit card, digital cash( this is a form of electronic currency that exists only in cyberspace….

Security and safety of e-Transactions:

1. Transaction risks: In e-business risk may arise for the seller or the buyer on account of default on order taking/giving, delivery as well as payment.

2. Data storage and transmission risk: Vital information may be stolen or modified to pursue some selfish motives or simply for fun. VIRUS (Vital Information Under Siege), Hacking, brand hijacking….. are some of risk in e-business.

3. Risk of threat to intellectual property and privacy: Once the information is published in internet, it is difficult to protect it from being copied.

Cryptography: It refers to the art of protecting information by transforming it into an unreadable format called cyphertext. Only those who possess a secret key can decrypt the message into plaintext.

Resources required for successful e-business implementation:

✔ Adequate computer with telecom network.

✔ Technically qualified and trained work force.

✔ Well developed websites.

✔ Well developed telecommunication facilities.

✔ A good system of making payments using credit instruments.

Outsourcing:

It refers to business organizations concentrate of their core activities and outsource other services to specialized agencies. The services which are commonly outsourced are financial services (it includes preparation of financial plans, issue of shares/debentures, raising funds ….), advertisement services (include designing messages, selecting models, media….), courier services (include mailing letters and parcels….), transportation (providing various transportation facilities), warehousing, after sales services etc.

Need/ Benefits/ Objectives of Outsourcing:

1. Focusing attention: Outsourcing helps the business to focus on its core activities and contracting out the rest.

2. Provide better service: It helps to provide better services to customers through specialization.

3. Cost reduction: Through division of labour and specialization, it helps to reduce the cost too. This happens due to the outsourcing partners as they deliver the same service to a number of organizations.

4. Growth through alliance: Through outsourcing firms investment requirements are reduced therefore they can expand rapidly.

5. Enhance economic development: Outsource stimulates entrepreneurship, employment and exports.